Paystack, the African payments company owned by Stripe, has sent a cease and desist notice to crypto startup Zap Africa after launching its new consumer product, Zap by Paystack.

This legal move comes in response to Zap Africa’s claims that Paystack failed to check whether “Zap” was already in use before branding their product.

The announcement of Paystack’s new offering stirred up a debate online, with Zap Africa accusing the payments giant of neglecting due diligence. But according to a source within Paystack, the company did its homework before moving forward with the name.

“We’re confident that we filed for trademark and that we filed in the right category,” the source told Condia. “We registered the [Zap] trademark across multiple classes, including financial services — a class where Zap Africa has no filing registration.”

Documents reviewed by Condia confirm that Paystack applied for a trademark on December 4, 2023, covering six different categories, including financial affairs, monetary services, insurance, and estate affairs. Meanwhile, a search of Nigeria’s Corporate Affairs Commission (CAC) registry shows that many businesses already use “Zap” in their names.

Zap Africa has also raised concerns that Paystack’s use of “Zap” is confusing its customers. However, the Paystack source dismissed this argument, pointing out that “Zap” is a common word used by multiple businesses in different industries.

“Zap” is a common term widely used in everyday language, making it difficult to associate exclusively with a single brand,” the source explained. “Over 40 companies listed on the CAC website include ‘Zap’ in their business names. Records from the Trademarks, Patents, and Designs Registry in Nigeria also show that the word ‘Zap’ has been in use for well over a decade. In fact, a trademark containing ‘Zap’ was filed as early as 2008 by an entirely different entity. So, the name is not exclusive to Zap Africa.”

It’s clear that this dispute is far from over, and how it unfolds could set a precedent for naming rights in Nigeria’s business landscape.

Dubai-based fintech startup Enza has just secured $6 million in seed funding to help African banks and fintechs improve their payment infrastructure.

Founded in 2022 by ex-Network International executives Hany Fekry and Hamish Houston, the company is stepping in to ensure traditional banks don’t get left behind in the fast-moving fintech revolution.

Fintech startups have shaken up Africa’s financial sector, offering fast, digital-first solutions that have left traditional banks struggling to keep up. Enza wants to change that by giving banks the tools they need to compete, not just survive.

How Enza Works

Enza’s platform is designed to support both sides of the payment process—issuing and acceptance. This means banks and fintechs can offer local payment solutions, including:

Card payments

Real-time transactions

Other digital payment methods

Rather than just focusing on merchant payments (like most processors do), Enza provides a full-scale solution that integrates seamlessly with existing financial systems. The company is starting with Egypt, Nigeria, and South Africa—three of Africa’s largest financial markets.

Why Payments Matter for Financial Inclusion

For small businesses across Africa, the ability to accept digital payments is often the first step toward financial growth. Enza’s strategy is built around two key benefits:

Key Benefit

How It Helps

Lower Costs for Businesses

Makes it easier for small businesses to accept digital payments.

Smarter Banking

Uses payment data to help banks offer lending, savings, and insurance products.

“Payments are the gateway, but the value is in the data and services you can layer on top,” said Enza executive director Andrew Key.

“Banks have realized they gave up too much ground to fintechs. We want to give them the tech to compete and win it back,” added co-founder Hamish Houston.

Even though fintech giants like Flutterwave and Moniepoint have made huge strides, banks still play a critical role in Africa’s financial ecosystem. They’re highly regulated and remain the backbone of payment networks. Enza helps them regain visibility and control over transactions while staying connected to major global and regional payment schemes like Visa, Mastercard, and others.

Enza is already making an impact, with:

Over 10 million monthly contracted transactions across six African markets, including Nigeria, Ghana, and South Africa.

35-40% month-over-month transaction growth, with plans to double volumes in two years.

Funding from Algebra Ventures and Quona Capital to expand its team and roll out new banking solutions across Africa.

“We founded Enza to solve real infrastructure problems,” said CEO Hany Fekry. “We want African communities to access financial products as easily as people in Europe or the U.S.”

With strong growth and investor backing, Enza is well on its way to reshaping Africa’s banking landscape. By giving banks the right tools, they’re making sure financial institutions can thrive in a world that’s increasingly going digital.

Moving money from your MTN MoMo wallet to your bank account in Ghana is easy once you know how. Whether you need to pay bills, save money, or send funds to a business account, this guide will show you three simple ways to get it done.

Let’s break it down step by step, so you can follow along without stress.

Method 1: Wallet-to-Bank Transfer (Direct Transfer)

This is the simplest way to move money from your MTN MoMo wallet to your bank. It requires that your MoMo wallet is linked to your bank account. Once linked, transferring money takes just a few steps.

Steps to transfer money using Wallet-to-Bank

Dial *170# on your phone.

Select Financial Services (usually option 5).

Choose Bank Services (option 1).

Select Transfer to Bank.

Choose your bank from the list.

If your bank is not listed, enter # to see more options.

Select the specific bank account you want to send money to.

You’ll receive a confirmation message when the transaction is successful.

Why use this method?

✅ No extra charges when your MoMo wallet is linked to your bank. ✅ Fast and convenient. ✅ Works with most major banks in Ghana.

Tip: If your bank account is not linked to your MoMo wallet, visit your bank to set it up for future transactions.

Method 2: GhIPSS Bank Transfer (For Unlinked Accounts)

If your MoMo wallet is not linked to your bank account, you can still send money using Ghana’s GhIPSS interoperability service. This method allows you to transfer money to any bank account, even if it’s not connected to MoMo.

Steps to transfer using GhIPSS

Dial *170# on your phone.

Select Transfer Money (option 1).

Choose Bank Account.

Select Wallet to Bank Account.

Pick the bank you want to send money to.

Enter the recipient’s bank account number.

Confirm the account number to avoid errors.

Enter the amount you want to transfer.

Type a reference note (e.g., “School Fees” or “Rent Payment”).

Enter your MoMo PIN to confirm the transfer.

You’ll receive a confirmation message.

Why use this method?

✅ Works even if your bank account is not linked to MoMo. ✅ Allows transfers to most banks in Ghana. ✅ Great for sending money to others who need a bank deposit.

Heads up: You’ll pay a small fee for this method

Method 3: Using Your Bank’s USSD Code

Some banks in Ghana have their own shortcodes (USSD codes) that allow you to transfer money from MoMo directly into your bank account. However, you must link your MoMo wallet to your bank first.

How to transfer using a bank USSD code

Dial your bank’s USSD code (e.g., *776# for Fidelity Bank, *422# for GCB).

Select the MoMo to Bank transfer option.

Enter the amount you want to send.

Confirm your account number.

Approve the transaction with your MoMo PIN.

Wait for a confirmation message.

Why use this method?

✅ You don’t need to dial *170# every time. ✅ Some banks offer additional transfer benefits. ✅ Fast and straightforward if you frequently send money to your bank.

MTN MoMo to Bank Transfer Charges

If you transfer money from your MoMo wallet to a bank that is not linked, you will pay a small fee. Below is a breakdown of charges:

Amount (GHS)

Charge (GHS)

E-Levy (1.5%)

0.01 – 50

0.38

No levy

50 – 100

0.75%

No levy

100 – 1,000

1.5%

Applied

Above 1,000

7.5

Applied

✅ Daily Tax-Free Limit: You can transfer up to GHS 100 per day without paying the E-Levy. ✅ No Charges for Linked Accounts: If your MoMo wallet is linked to your bank, you can transfer money for free using Method 1.

Important Security Tips for MoMo Transfers

When using MoMo to send money to a bank, always prioritize security. Here’s how:

✔ Keep your MoMo PIN secret – Never share it with anyone, not even MTN staff. ✔ Verify recipient details – Always double-check the bank account number before confirming the transfer. ✔ Watch out for scams – Be cautious of messages or calls asking for your MoMo details. ✔ Report suspicious activity – If you suspect fraud, contact MTN customer support immediately.

Transferring money from MTN MoMo to a bank in Ghana is simple when you know the right steps. Whether you use the direct Wallet-to-Bank method, GhIPSS, or your bank’s USSD code, the process is fast and reliable.

If you want free transfers, make sure your MoMo wallet is linked to your bank. But if you need to send money to a different account quickly, GhIPSS and bank USSD codes are great alternatives.

Now that you know how it works, go ahead and transfer money with confidence!

FAQs

How long does it take for an MTN MoMo bank transfer to reflect in my account?

Transfers from MTN MoMo to a bank account are typically processed instantly. However, in some cases, it may take up to 24 hours, depending on your bank’s processing time.

What are the transaction limits for MTN MoMo bank transfers?

The limits for sending money from MTN MoMo to a bank account vary based on your account type:

Account Type

Daily Limit (GHS)

Monthly Limit (GHS)

Minimum

3,000

10,000

Medium

15,000

Unlimited

Enhanced

25,000

Unlimited

Keep in mind that banks may have their own transfer limits. It’s best to check with your bank for any additional restrictions.

Are there any fees for transferring money from MTN MoMo to a bank account?

Yes, MTN MoMo charges a small transaction fee when sending money to a bank account. The fee varies based on the transfer amount and is deducted at the time of the transaction. You can check the exact charges within the MoMo app or by dialing the MoMo service code.

Can I cancel a bank transfer after initiating it?

Once a transfer has been processed, it cannot be reversed. If the money has not yet been credited to the recipient’s account, you may contact MTN MoMo customer support for assistance, but a reversal is not guaranteed.

Sending money to Nigeria should be simple, safe, and fast. Whether you’re supporting family, paying for services, or handling business transactions, choosing the right platform matters. But with so many options, how do you know which one to pick? No worries—I’ve got you covered. Let’s break it down in a way that makes sense, just like explaining a game plan to a friend.

Key Features of a Reliable Money Transfer Platform

Before diving into the list, here’s what we should look for in a good money transfer service:

Security – Your money should be safe from fraud and scams.

Speed – Some transfers are instant, while others take days.

Fees – Look for low or no fees.

Exchange Rates – Some services give better rates than others.

Ease of Use – It should be simple to send money without headaches.

Payment Methods – Options should include bank transfers, mobile wallets, and cash pickups.

Now, let’s explore 12 trusted platforms that make sending money to Nigeria easy and reliable.

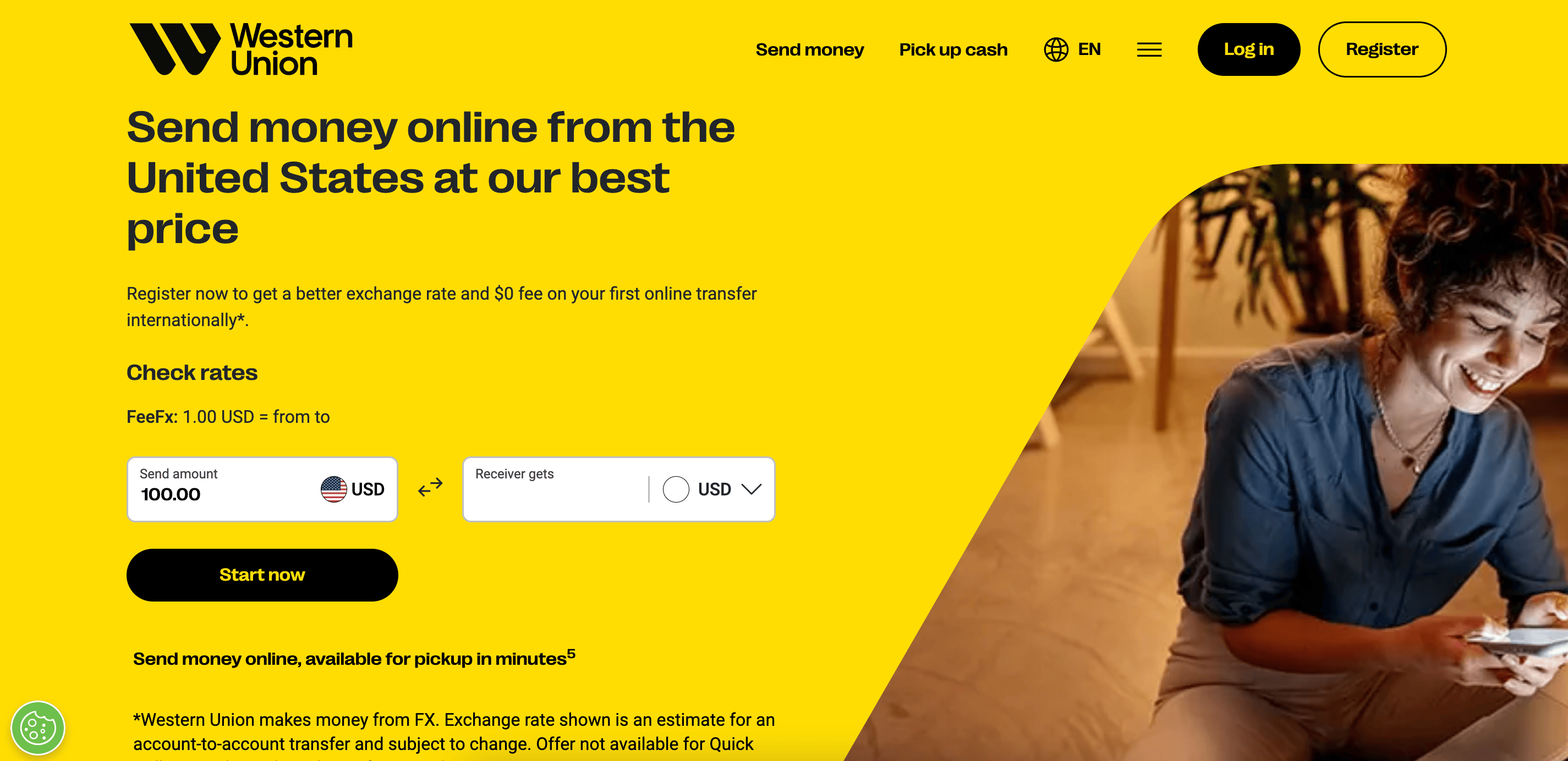

1. Western Union

Why it’s great:

Western Union has a large global network with thousands of locations.

Supports bank deposits, cash pickup, and mobile money.

Flexible payment options, including credit/debit cards and bank transfers.

Best for: Sending money to someone who prefers picking up cash in person.

2. MoneyGram

Why it’s great:

Fast and available worldwide.

Supports cash pickup, mobile money, and bank deposits.

Available in many retail locations, making it easy to send money.

Best for: Those who prefer in-person transactions or need fast cash pickups.

3. Remitly

Why it’s great:

Express (instant) and Economy (cheaper but slower) options.

Supports mobile money, bank deposits, and cash pickup.

Offers promotional exchange rates for first-time users.

Best for: First-time senders looking for a good deal and reliable delivery options.

4. WorldRemit

Why it’s great:

Supports bank deposits, mobile money, and cash pickups.

Fast delivery, often within minutes.

Reasonable fees with competitive exchange rates.

Best for: Sending money in multiple ways, especially for cash pickups and mobile wallets.

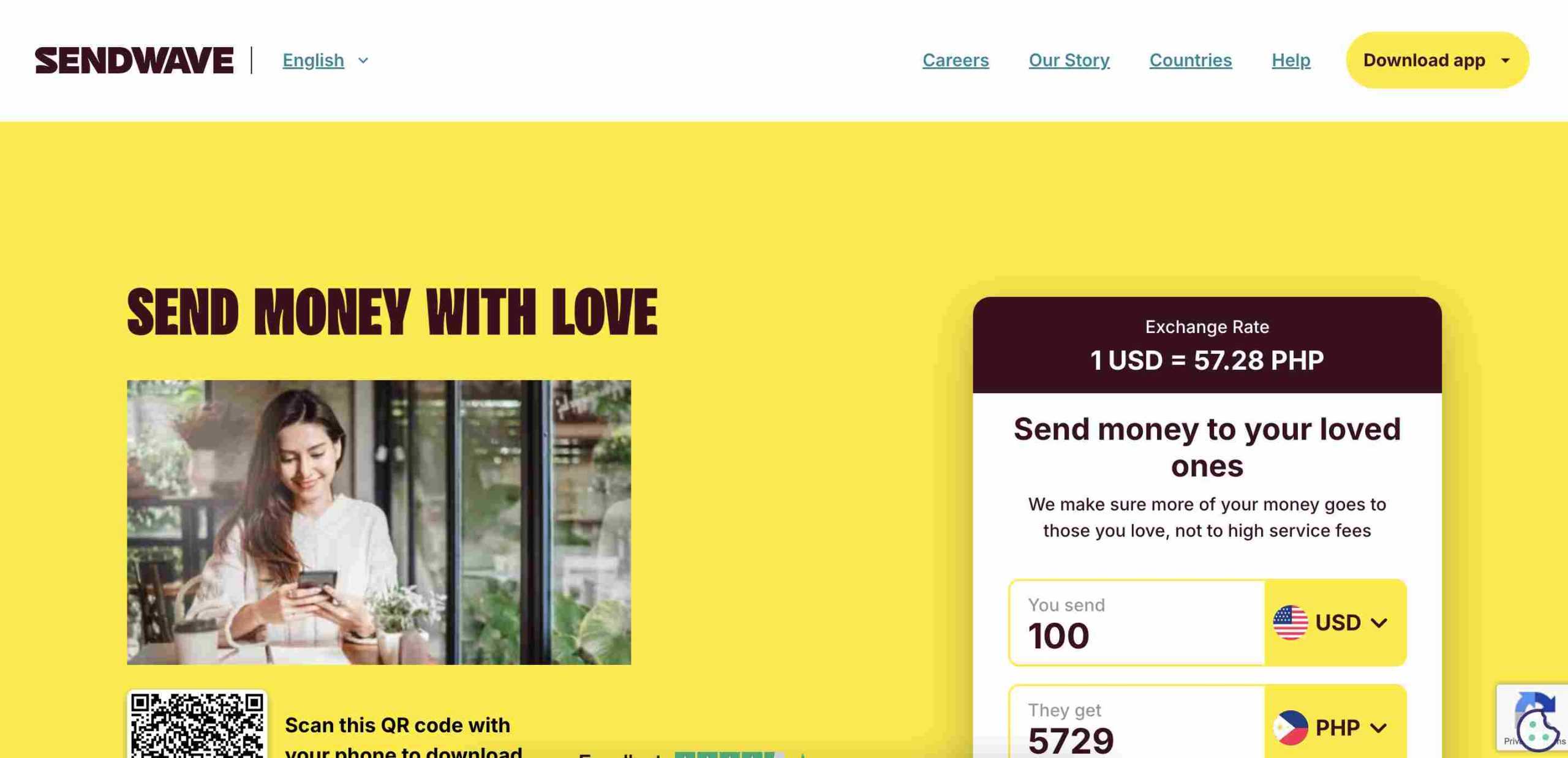

5. Sendwave

Why it’s great:

No fees for transfers.

Fast transfers, often within minutes.

Sendwave works with mobile money services like Opay and PalmPay.

Easy to use with a mobile app.

Best for: People who want quick, fee-free transfers straight to a mobile wallet.

Works well for Nigerians in the diaspora sending money home.

Best for: People looking for fee-free international transfers with multi-currency support.

9. Paysend

Why it’s great:

Flat transfer fee of about $2.

Direct transfers to bank accounts and mobile wallets.

Fast transactions, often within minutes.

Best for: Those who want low-cost international transfers with simple pricing.

10. Skrill

Why it’s great:

Allows sending money using a digital wallet.

Low-cost transactions compared to traditional banks.

Works well for online purchases and payments as well.

Best for: Digital-savvy users who want a multi-purpose wallet for sending money and online transactions.

11. TransferGo

Why it’s great:

Fast transfers, sometimes as quick as 30 minutes.

Competitive exchange rates.

Supports bank deposits.

Best for: Those who need quick transfers to a bank account with good exchange rates.

12. Remitbee

Why it’s great:

No fees for bank transfers over $500.

Good exchange rates compared to banks.

Remitbee works well for Canadians sending money abroad.

Best for: People in Canada who want affordable and reliable transfers.

Comparing the Best Options

Here’s a quick comparison to help you choose the right service:

Platform

Fees

Speed

Payment Methods

Best For

Western Union

Varies

Fast

Bank, mobile, cash

Cash pickups worldwide

MoneyGram

Varies

Fast

Bank, mobile, cash

In-person and urgent transfers

Remitly

Low

Varies

Bank, mobile, cash

First-time users & flexible options

WorldRemit

Low

Fast

Bank, mobile, cash

Multiple transfer options

Sendwave

No

Fast

Mobile money

Instant, fee-free transfers

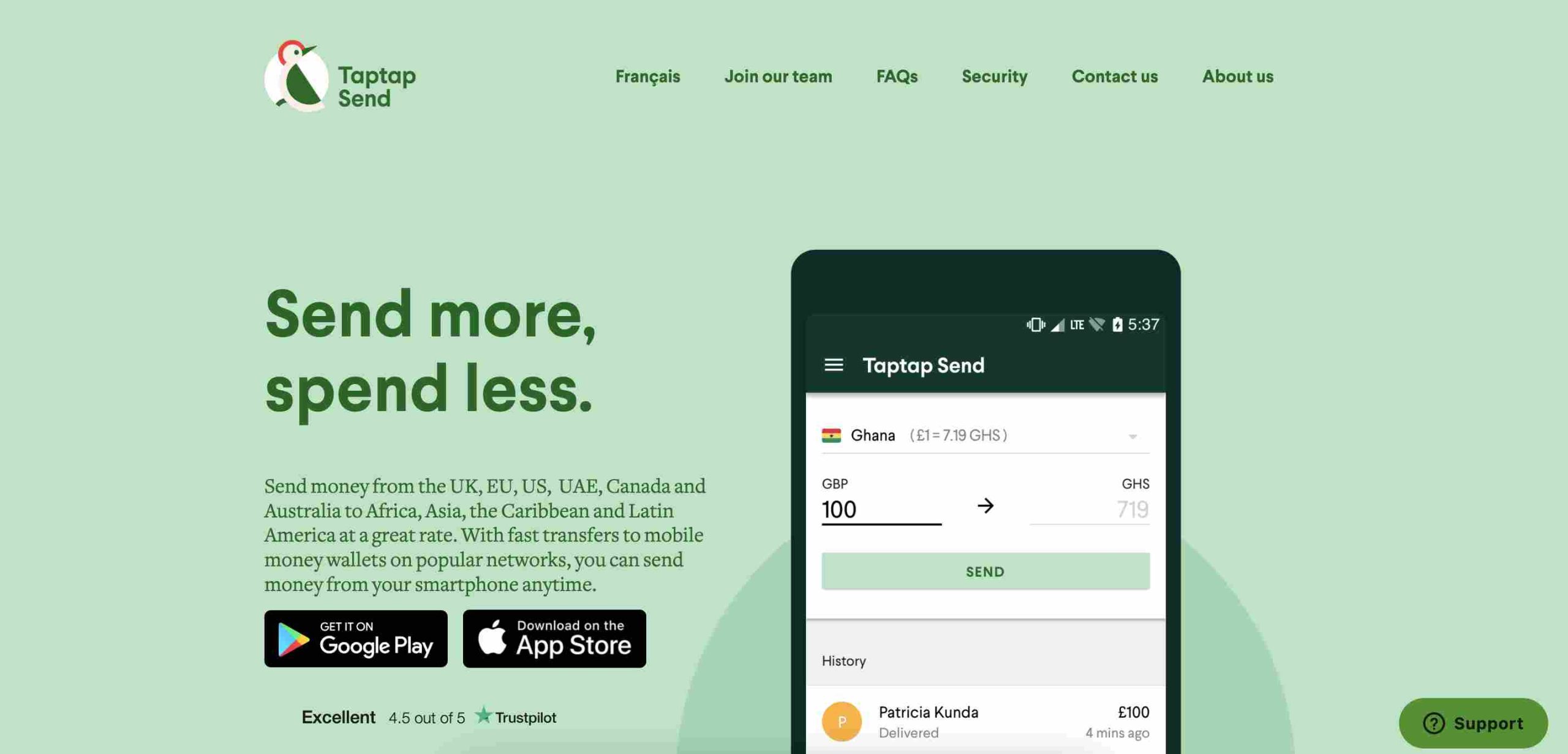

Taptap Send

No

Fast

Mobile money

Fee-free mobile money transfers

ACE Money Transfer

Low

Fast

Bank, mobile, cash

Competitive exchange rates

LemFi

No

Fast

Multi-currency

No-fee transfers

Paysend

$2

Fast

Bank, mobile

Low-cost transfers

Skrill

Low

Fast

Digital wallet

Online payments & money transfers

TransferGo

Low

Fast

Bank deposits

Quick bank transfers

Remitbee

No (over $500)

Fast

Bank deposits

Canadians sending money

Your choice of money transfer platform depends on what matters most—speed, cost, or payout methods. For no-fee mobile transfers, Sendwave and Taptap Send are excellent options. If you prioritize favorable exchange rates, TransferGo or ACE Money Transfer might be the best fit. And for those who need cash pickup, Western Union or MoneyGram could be the right solution. No matter which you choose, all these platforms are secure and trustworthy for sending money to Nigeria.

Sending money to South Africa should be easy, secure, and fast. Whether you’re supporting family, paying for services, or handling business transactions, picking the right platform is essential. With so many options, how do you choose the best one? Don’t worry—I’ve got you covered. Let’s break it down in a way that makes sense, like explaining a game plan to a friend.

How to Identify a Good Money Transfer Platform

Before we jump into the list, here’s what to look for in a reliable money transfer service:

Security – Your money should be protected from fraud and scams.

Speed – Some transfers happen instantly, while others take a few days.

Fees – Look for low or no fees to save on costs.

Exchange Rates – Some platforms offer better rates than others.

Ease of Use – The platform should be simple to navigate.

Payment Methods – Options should include bank transfers, mobile wallets, and cash pickups.

Now, let’s explore 12 trusted platforms that make sending money to South Africa seamless and secure.

1. Western Union

Why it’s great:

Large global network with thousands of locations.

Western Union supports bank deposits, cash pickup, and mobile money.

Multiple payment options, including credit/debit cards and bank transfers.

Best for: Sending money to someone who prefers picking up cash in person.

Fast and direct deposits to mobile money accounts.

Easy-to-use mobile app for seamless transfers.

Best for: Mobile money users who want quick and free transfers.

11. LemFi

Why it’s great:

Zero transaction fees.

Supports multiple currencies for international transfers.

LemFi works well for South Africans living abroad who send money home frequently.

Best for: People who want fee-free international transfers with multi-currency support.

12. Remitbee

Why it’s great:

No fees for bank transfers over $500.

Strong exchange rates compared to banks.

Remitbee is ideal for Canadians sending money abroad.

Best for: Those in Canada who need a reliable and affordable way to send money to South Africa.

Comparing the Best Options

Here’s a quick comparison to help you pick the right service:

Platform

Fees

Speed

Payment Methods

Best For

Western Union

Varies

Fast

Bank, mobile, cash

Cash pickups worldwide

MoneyGram

Varies

Fast

Bank, mobile, cash

In-person and urgent transfers

WorldRemit

Low

Fast

Bank, mobile, cash

Multiple transfer options

Remitly

Low

Varies

Bank, mobile, cash

First-time users & flexible options

Paysend

$2

Fast

Bank, mobile

Low-cost transfers

Skrill

Low

Fast

Digital wallet

Online payments & money transfers

TransferGo

Low

Fast

Bank deposits

Quick bank transfers

ACE Money Transfer

Low

Fast

Bank, mobile, cash

Competitive exchange rates

Sendwave

No

Fast

Mobile money

Instant, fee-free transfers

Taptap Send

No

Fast

Mobile money

Fee-free mobile money transfers

LemFi

No

Fast

Multi-currency

No-fee transfers

Remitbee

No (over $500)

Fast

Bank deposits

Canadians sending money

The best money transfer platform for you depends on what matters most—speed, cost, or payout methods. For fee-free mobile transfers, Sendwave and Taptap Send are solid options. If you’re after competitive exchange rates, consider TransferGo or ACE Money Transfer. Need cash pickup? Western Union or MoneyGram may be the best fit.

Whichever platform you choose, you can be confident that all of these are safe and reliable options for sending money to South Africa.

Sending money to Ghana should be simple, safe, and fast. Whether you’re supporting family, paying for services, or handling business transactions, choosing the right platform matters. But with so many options, how do you know which one to pick? No worries—I’ve got you covered. Let’s break it down in a way that makes sense, just like explaining a game plan to a friend.

What Makes a Good Money Transfer Platform?

Before diving into the list, here’s what we should look for in a good money transfer service:

Security – Your money should be safe from fraud and scams.

Speed – Some transfers are instant, while others take days.

Fees – Look for low or no fees.

Exchange Rates – Some services give better rates than others.

Ease of Use – It should be simple to send money without headaches.

Payment Methods – Options should include bank transfers, mobile wallets, and cash pickups.

Now, let’s explore 12 secure platforms that make sending money to Ghana easy and reliable.

1. Sendwave

Why it’s great:

No fees for transfers.

Fast transfers, often within minutes.

Sendwave works with mobile money services like MTN and Vodafone Cash.

Easy to use with a mobile app.

Best for: People who want quick, fee-free transfers straight to a mobile wallet.

Choosing the right platform depends on what matters most to you—whether it’s speed, fees, or payout options. If you want no-fee mobile transfers, Sendwave or Taptap Send are great choices. Need a good exchange rate? TransferGo or ACE Money Transfer could be your best bet. And if cash pickup is important, Western Union or MoneyGram might work better.

No matter which one you choose, rest easy knowing these are all secure and trusted ways to send money to Ghana.

Online banking is changing the way Nigerians save, spend, and manage their money. Whether you’re looking for a bank with free transfers, instant loans, or high savings interest rates, there’s an option for you. This guide breaks down the best online banks in Nigeria, making it easy to choose the one that fits your needs.

What Makes a Great Online Bank?

Before we dive into the list, here are key things to look out for when choosing an online bank:

Security: The bank should have strong security features like two-factor authentication (2FA) and encryption to keep your money safe.

Ease of Use: A simple and user-friendly mobile app is a must.

Low or No Fees: Many online banks offer free transfers and zero maintenance fees.

Savings & Loans: Some banks offer high-interest savings and quick loans.

Reliable Customer Support: You need a bank that responds fast when you have issues.

Now, let’s explore the best online banks in Nigeria.

1. Kuda

Kuda is one of the most popular online banks in Nigeria, offering a smooth, fee-free banking experience.

Key Features:

Free monthly transfers (up to 25)

Automated savings with competitive interest rates

Instant loans with no collateral

Investment options through Bamboo integration

Best For: People who want a free, easy-to-use digital bank with savings and loan features.

2. PalmPay

PalmPay is a digital wallet that makes everyday transactions easy and rewarding.

Key Features:

Cashback and discounts on transactions

Quick and simple registration

Free and low-cost transfers

Best For: Anyone looking for a simple digital wallet with rewards.

3. Sparkle

Sparkle is a modern digital bank offering personal and business banking.

Key Features:

Smart spending insights and analytics

Business banking features for entrepreneurs

Virtual and physical debit cards

Best For: Freelancers and small business owners who need banking and financial insights.

4. FairMoney

FairMoney started as a loan app but has expanded into a full online bank.

Key Features:

Quick, collateral-free loans

Bill payments and mobile top-ups

Free bank transfers

Best For: Anyone who frequently needs instant loans.

5. ALAT by Wema

ALAT is a pioneer in Nigeria’s online banking space, offering a full range of services.

Best For: Business owners and people who need a reliable payment system.

13. VFD Bank

VFD Bank is a flexible online bank with great savings and budgeting features.

Key Features:

Up to 10% interest on savings

Free transfers

Joint and kids’ accounts

Best For: Savers and professionals who need a high-interest digital bank.

Choosing the Right Online Bank

Here’s a quick comparison to help you pick the best online bank for your needs:

Bank

Best For

Free Transfers

Instant Loans

High-Interest Savings

Kuda Bank

Personal Banking

✅

✅

✅

PalmPay

Cashback Rewards

✅

❌

❌

Sparkle

Business & Personal Insights

✅

❌

✅

FairMoney

Instant Loans

✅

✅

❌

ALAT

International Payments

✅

✅

✅

PocketApp

Social Savings

✅

❌

✅

Sofri

Simple Banking

✅

❌

✅

OPay

Multifunctional Use

✅

❌

❌

Carbon

Loans & Savings

✅

✅

✅

Paga

USSD Banking

✅

❌

❌

Eyowo

Easy Access

✅

❌

❌

Moniepoint

Business Banking

✅

❌

❌

VFD Bank

High Interest Savings

✅

❌

✅

Online banking in Nigeria is growing fast, and these digital banks are leading the way. Whether you need free transfers, easy loans, or high-interest savings, there’s an online bank for you. Before choosing, consider what features matter most to you and pick the one that fits your lifestyle best.

FAQs:

1. Which online bank is the most reliable in Nigeria?

Reliability depends on what you need. Kuda, OPay, and PalmPay are among the most reliable online banks due to their ease of use, fast transactions, and good customer service. Moniepoint is also highly reliable, especially for businesses.

2. Can a 13-year-old have a bank account in Nigeria?

Yes, but only with a parent or guardian. Most banks, including online ones, require minors to open an account under parental supervision. Some banks offer special accounts for kids and teens, but full banking services are usually available from age 16 or 18.

3. What is the most trusted online bank?

Kuda, ALAT by Wema, and FairMoney are among the most trusted online banks. Kuda is known for zero maintenance fees, ALAT is backed by Wema Bank, and FairMoney is popular for quick loans.

4. Which is the most trusted bank in Nigeria?

For traditional banks, Zenith Bank, GTBank, and First Bank are considered the most trusted. Among digital banks, Kuda and Moniepoint are highly rated for security and reliability.

5. Does Kuda allow under 18?

No, Kuda requires users to be at least 18 years old to open an account.

6. At what age can I open an OPay account?

OPay allows users from 18 years and above to open an account.

7. Does Kuda need NIN?

Yes, Kuda requires a National Identification Number (NIN) or another valid ID for account verification.

8. What is the banking app for 15-year-olds in Nigeria?

Most online banks in Nigeria require users to be at least 18. However, some traditional banks like GTBank and Access Bank offer teen accounts that can be managed with a parent or guardian.

Investing is one of the smartest ways to grow your money, but with so many platforms available, it can be overwhelming to decide where to start. Whether you’re looking for stocks, mutual funds, real estate, or even cryptocurrency, there’s an investment platform in Nigeria for you. Let’s break it down in a simple, easy-to-follow way.

1. Bamboo

Bamboo allows Nigerians to invest in U.S. and Nigerian stocks right from their phones. You can buy shares in companies like Apple, Tesla, and Amazon with as little as $10. Bamboo also offers a “US Wallet” feature that lets you hold your funds in dollars, protecting them from naira depreciation.

Key Features:

Invest in Nigerian and U.S. stocks

Fractional shares available (own a piece of a stock)

SEC-regulated for security

Real-time market data

2. Chaka

Chaka provides access to over 4,000 stocks across Nigeria and international markets. If you want to diversify your investments, Chaka is a great choice. It allows you to open dollar and naira accounts, making it flexible for different currencies.

Key Features:

Invest in Nigerian, U.S., and global stocks

SEC-licensed for safety

Knowledge Base for beginners

3. Risevest

Risevest is a great option if you want professionals to manage your investments. They offer portfolios in U.S. stocks, real estate, and fixed-income assets. This is perfect for people who prefer a hands-off approach.

Key Features:

Professional portfolio management

Invest in U.S. stocks, real estate, and bonds

No Nigerian stock options

4. PiggyVest

PiggyVest, co-founded by Odunayo Eweniyi, one of Nigeria’s top tech women, started as a savings platform but has expanded to offer investment options. It allows users to invest in real estate, government bonds, and other assets with as little as ₦5,000.

Trove offers a mix of traditional and digital investments. With Trove, you can invest in Nigerian and global stocks, ETFs, bonds, and even cryptocurrencies.

Key Features:

Over 10,000 investment options

Start with as little as ₦1,000 or $10

Includes cryptocurrency investments

6. Cowrywise

Cowrywise is designed for those who want to automate their savings and investments. It focuses on mutual funds and does not offer stocks, making it great for long-term wealth building.

Key Features:

Invest in low, medium, and high-risk mutual funds

Automated savings feature

Investment circles for group investing

7. Quidax

If you’re interested in Bitcoin, Ethereum, and other digital currencies, Quidax is a great option. It offers a simple way to buy, sell, and store crypto assets.

Key Features:

Easy-to-use crypto trading platform

Secure wallet for storing digital assets

Approved by the Nigerian SEC

8. I-Invest

I-Invest is best for those looking for safe, low-risk investments like Treasury bills, Eurobonds, and mutual funds.

GetEquity allows you to invest in startups and high-growth companies in Africa. This is a high-risk, high-reward investment option.

Key Features:

Invest in early-stage African startups

Venture capital and equity funding

High potential returns

10. Crowdyvest

Crowdyvest focuses on funding impactful projects in sectors like agriculture, real estate, and transportation. This is perfect for those who want their investments to drive social change.

Key Features:

Invest in agriculture, real estate, and transport projects

When choosing an investment platform, consider the following:

Your Goals: Do you want short-term or long-term returns? Stocks and real estate are great for long-term growth, while Treasury bills offer stability.

Risk Tolerance: Are you comfortable with high-risk investments like crypto and startups, or do you prefer safe options like bonds?

Platform Fees: Some platforms charge transaction fees, while others take a percentage of your profits.

Ease of Use: Beginners may prefer user-friendly platforms like PiggyVest or Cowrywise.

FAQs

What is the best investment platform in Nigeria?

It depends on your goals. Bamboo and Chaka are great for stocks, while PiggyVest and Cowrywise are best for beginners. If you want cryptocurrency, Quidax is a strong option.

Can I invest in U.S. stocks from Nigeria?

Yes! Platforms like Bamboo, Chaka, and Trove allow Nigerians to invest in U.S. stocks.

Are these investment platforms safe?

Yes, most are regulated by the Securities and Exchange Commission (SEC). However, always do your research before investing.

What’s the minimum amount needed to start investing?

You can start with as little as ₦1,000 on Trove, while others require ₦5,000 or more.

There’s no one-size-fits-all investment platform. The best one for you depends on your financial goals, risk appetite, and investment interests. Whether you’re looking for stocks, bonds, real estate, or crypto, Nigeria has an investment platform for you. Start small, stay consistent, and watch your money grow!

In today’s digital world, having access to a virtual dollar card has become essential for Nigerians who want to shop online, subscribe to international services, or run a global business. These cards solve a major problem: how to spend money internationally without the hassle and high fees of traditional banking.

What Are Virtual Dollar Cards?

Think of a virtual dollar card as a digital version of a physical credit or debit card. It works exactly the same way – you can use it to make purchases online – but it exists only in digital form. You get all the card details (card number, expiry date, and CVV) without having a piece of plastic in your wallet.

These cards are funded with dollars, which means you can pay for services that only accept USD without worrying about currency conversion issues. For Nigerians dealing with services like Netflix, Spotify, Amazon, or platforms that require dollar payments, these cards are a game-changer.

Why Nigerians Need Virtual Dollar Cards

If you’ve ever tried to use a Nigerian naira card for international purchases, you might have encountered frustrating declines or restrictions. Virtual dollar cards solve several problems:

Global Acceptance: They work on platforms that might reject Nigerian cards

Forex Simplicity: You avoid complicated currency conversion processes

Lower Fees: Many virtual card providers offer better rates than traditional banks

Security: You can create and delete cards as needed, reducing fraud risk

Subscription Management: Perfect for managing recurring payments to international services

Top Virtual Dollar Cards in Nigeria Now

Let’s dive into the best options available for Nigerians right now. I’ve researched the top providers and compiled their key features to help you find your perfect match.

Top Selection at a Glance

Provider

Creation Fee

Monthly Fee

Min Funding

Monthly Limit

Special Features

Cardtonic

$1.5

none

Not specified

Not specified

Best exchange rates, widely accepted

Vesti

$10

none

$10

$10,000

100+ platform acceptance

GeePay

$3

none

$2

Not specified

Multiple currencies (USD, GBP, EUR)

Grey

$4 ($1 rebate)

none

$2

$2,500/transaction

Multi-currency support

Chipper Cash

$3

$1

Not specified

Not specified

3D-secure protection

Cardify Africa

$2

none

Not specified

Not specified

Multiple funding options

PSTNET

$7-$10

none

Not specified

Not specified

Specialized for ads platforms

Zole

$2

none

Not specified

Not specified

0.5% transaction fee, 3-year validity

Klasha

$2

none

Not specified

Not specified

Spending analytics

Bitsika

$3

none

Not specified

Not specified

Crypto & Naira funding

Dantown

$2

none

Not specified

Not specified

Crypto & Naira funding

Changera

Varies

none

$0

$10,000

Multi-currency support

ALAT by Wema

none

none

Not specified

Not specified

Bank-backed security

Spectrocard

$3

none

Not specified

Not specified

Detailed transaction reports

Tribapay

Varies

none

Not specified

Not specified

Multiple cards, PayPal linking

Fundall

Free (1st card), $2 (others)

none

$5

Not specified

Multiple card creation

Bitnob

$1

$1 (if < $100)

Variable

$10,000

Customizable cards

Eyowo

$2

none

Not specified

Not specified

Spending tracking

Eversend

none

$1

$1

Not specified

Multi-country support

Gomoney

Free (1st card), ₦850 (others)

none

Not specified

$100

Free first card

Nearpays

$2

none

Not specified

Not specified

Spending limits feature

PayDay

$2

none

$2

Not specified

Integrated with financial tools

Kuda

Free

none

$1

$1,000

No maintenance fees

Note: Information is accurate as of this article’s publication. Some details may change, so always check the provider’s website for the most current information.

Cardtonic offers one of the most affordable virtual dollar cards in Nigeria with wide acceptance across major platforms. The card can be funded in Naira at competitive exchange rates, making it ideal for international payments. No recurring fees make it a cost-effective option for regular users.

Why Cardtonic stands out:

Global acceptance on major platforms including Amazon, Netflix, Spotify, ChatGPT, and more

Simple setup process: just download the app, complete KYC, and fund your wallet

Perfect combination of affordability, ease of use, and reliability

The absence of maintenance fees means you’re not paying for the card when you’re not using it

For beginners just getting started with virtual dollar cards, Cardtonic offers an ideal entry point with its user-friendly approach and comprehensive platform support.

2. Vesti

If you’re looking to make larger international payments, Vesti deserves your attention. With a monthly spending limit of $10,000, it’s built for users who need to move significant amounts.

Minimum Funding: $10 Monthly Limit: $10,000 Standout Feature: Accepted on over 100 platforms

Vesti’s virtual dollar card offers a straightforward experience with strong security features. The app lets users easily manage transactions, view balances, and delete compromised cards when necessary. It’s particularly good for users who want reliability without complexity.

What makes Vesti special:

User-friendly app interface for easy transaction management

Secure payment processing with reliable customer support

High monthly spending limit ideal for business transactions

Comprehensive platform support for various international services

Vesti is particularly suitable for business owners and professionals who need higher transaction limits and robust security features.

3. GeePay (by Raenest)

GeePay takes flexibility to another level by offering virtual cards in multiple currencies (USD, GBP, and EUR). This makes it perfect for freelancers and business owners who work with clients from different regions.

Perfect for freelancers and business owners, GeePay’s card works seamlessly with platforms like PayPal and Payoneer. The multi-currency support makes it versatile for various international transactions. It also supports withdrawals to local banks and mobile money accounts in over 100 countries.

GeePay’s standout features:

No monthly maintenance charges

Works seamlessly with PayPal and Payoneer

Supports withdrawals to local banks in over 100 countries

Ideal for freelancers working with international clients

If you’re a freelancer receiving payments from clients abroad, GeePay offers the currency flexibility that can save you money on conversion fees.

4. Grey

Grey offers an interesting proposition: a $4 creation fee but gives you $1 back into your account. This effectively makes the creation cost just $3, along with zero maintenance fees.

Creation Fee: $4 (with $1 cashback) Funding Range: $2 – $2,500 per transaction Standout Feature: Zero maintenance fees with competitive exchange rates

Grey offers flexible funding options with support for multiple currencies including NGN, USD, and GBP. The absence of maintenance fees makes it economical for long-term use. Its simplicity and reliability make it a top choice.

Grey’s advantages:

Multi-currency support (NGN, USD, GBP)

Competitive exchange rates

Seamless user experience with intuitive app design

Effective $3 creation fee after cashback

Grey is ideal for regular online shoppers who want a straightforward, no-hidden-fees experience for their international purchases.

5. Chipper Cash

Security-conscious users will appreciate Chipper Cash‘s 3D-secured virtual dollar card. While it does come with a $1 monthly maintenance fee (one of the few on this list that charges monthly), the enhanced security features make it worthwhile for many.

Chipper Cash provides enhanced security with 3D protection, making it a safe option for international payments. The strong acceptance on popular platforms like Spotify, Netflix, and Apple services makes it worth considering. The app offers a user-friendly interface for managing your card.

Why consider Chipper Cash:

Strong security features with 3D authentication

Wide acceptance on popular platforms

User-friendly mobile app for card management

Reliable customer support

If security is your primary concern when making online payments, the small monthly fee might be a worthwhile trade-off for Chipper Cash’s enhanced protection.

Cardify Africa‘s virtual dollar card offers flexibility and ease of use. The zero maintenance fee policy keeps costs down for regular users, and the multiple funding options make it accessible regardless of how you prefer to manage your money.

The card works well on platforms like AliExpress, eBay, and Amazon, giving you access to a world of online shopping without the typical restrictions Nigerian cards face.

7. PSTNET

Monthly Fee: $7-$10 Standout Feature: Specialized cards for advertising and e-commerce

PSTNET‘s cards are specifically designed for users who need to run digital advertising campaigns or make specialized online purchases. Though the fees are higher than some competitors, the specialized nature of these cards makes them invaluable for businesses running campaigns on platforms like Facebook Ads, TikTok, and Google.

You can fund the card with cryptocurrency, and the app offers tools to track spending and download transaction histories. If you’re running digital marketing campaigns, the specialized features justify the higher cost.

8. Zole

Creation Fee: $2 Validity: 3 years Standout Feature: Long validity period with no maintenance fees

Zole offers excellent value with a three-year validity period and no recurring maintenance costs. The 0.5% transaction charge is transparent and reasonable for the service provided. It’s particularly good for educational platforms like Udemy and Coursera.

If you’re looking for a card you can set up once and use for years without worrying about renewal fees, Zole provides an attractive option.

Klasha combines affordability with powerful features like spending analytics, real-time transaction notifications, and detailed histories. The competitive exchange rates when funding from your Naira wallet make it an economical choice for regular international shoppers.

The app also keeps you organized with spending analytics, making it perfect for budget-conscious users who want to track their international spending habits.

Bitsika offers flexibility with its funding options, accommodating both traditional currency users and crypto enthusiasts. The absence of maintenance charges and the intuitive app interface make it a solid choice for managing international payments.

If you’re into cryptocurrency and want the option to fund your card directly from your crypto holdings, Bitsika provides a seamless experience for bridging the crypto and fiat worlds.

Dantown provides a reliable virtual dollar card that works well with major international platforms including the sometimes-challenging PayPal. The dual funding options (Naira or cryptocurrency) offer flexibility for different types of users.

For Nigerians who need reliable PayPal access, Dantown solves a common pain point with its compatibility with the platform.

Changera, powered by Bitmama, offers excellent flexibility with its multi-currency support. The absence of a minimum funding requirement removes barriers for new users, and the compatibility with PayPal makes it versatile for various uses.

The high monthly limit of $10,000 also makes it suitable for business users who need to make larger transactions.

13. ALAT by Wema

Standout Feature: Bank-backed security and integration

As a product of an established bank, ALAT‘s virtual card offers enhanced security and reliability. The seamless integration with the bank’s other services provides a comprehensive financial experience, and the ability to quickly manage cards within the app adds convenience.

If you already use Wema Bank services, the integration with your existing banking relationship makes ALAT a natural choice.

Spectrocard caters especially well to business owners and freelancers who need detailed transaction reports. The multiple funding options and absence of hidden charges make it transparent and user-friendly.

Business owners will appreciate the ability to download detailed transaction reports directly from the app, simplifying expense tracking and financial management.

15. Tribapay

Standout Feature: Multiple card creation and PayPal linking

Tribapay excels in flexibility, allowing users to create multiple cards for different purposes. The ability to link cards to PayPal accounts and set individual spending limits offers enhanced control over your finances.

If you need to separate spending for different projects or clients, Tribapay’s multiple card management features provide the organization you need.

16. Fundall

First Card: Free Additional Cards: $2 each Minimum Funding: $5 Standout Feature: First card free policy

Fundall offers excellent value with its free first card policy. The minimum funding requirement is reasonable, and the broad acceptance across major platforms makes it versatile for various uses.

For newcomers to virtual dollar cards, the zero entry cost makes Fundall an attractive option to test the waters without financial commitment.

Bitnob stands out with its highly customizable cards and remarkably low creation fee. The card works across several African countries, making it a good option for regional transactions as well as international ones.

The personalization options let you create cards that reflect your personality or business brand, adding a unique touch to your financial tools.

Eyowo combines simplicity with security, offering competitive exchange rates when funding with Naira. The tracking and card management features in the app add valuable control for users.

The app makes life easier by letting you track spending, freeze your card, or delete it if necessary, giving you complete control over your card security.

Eversend‘s broad geographic support makes it ideal for users who transact across multiple regions. The transparent fee structure and security features offset the small monthly maintenance fee.

The multi-country support makes it particularly valuable for users who travel frequently or do business across different regions.

20. Gomoney

First Card: Free Additional Cards: ₦850 each Monthly Limit: $100 per user Standout Feature: Free first card with transparent spending breakdown

Gomoney is budget-friendly with its free first card policy and absence of monthly fees. The spending breakdown feature helps with financial management, though the $100 monthly limit may be restrictive for heavy users.

The transparent spending breakdown helps you understand where your money is going, making it ideal for budget-conscious users who want to keep track of their expenses.

Nearpays caters well to freelancers and businesses dealing with international clients. The spending limit features and ability to freeze cards add security and control that professional users will appreciate.

The ability to set spending limits makes it perfect for budgeting and financial management, especially for freelancers with variable income.

PayDay offers a comprehensive financial experience by integrating its virtual card with broader financial planning tools. The low minimum funding requirement makes it accessible to new users, and the absence of monthly fees keeps costs predictable.

If you’re looking to incorporate your virtual card into a broader financial management strategy, PayDay’s integrated approach provides valuable synergy.

Kuda offers a virtual card with no creation fee, making it an affordable option for users looking for a cost-effective digital payment solution. With its low minimum funding requirement and absence of maintenance fees, Kuda is an attractive choice for those who want a seamless online transaction experience.

For individuals who need a hassle-free virtual card for everyday purchases, Kuda provides a straightforward and budget-friendly option without unnecessary charges.

How To Choose The Right Virtual Dollar Card

With so many options, how do you pick the right one? Here’s a simple framework:

Consider your usage pattern: Do you need it for occasional purchases or regular subscriptions?

Evaluate the fees: Look at creation fees, maintenance charges, and transaction costs

Check funding options: Do you prefer funding with Naira or cryptocurrency?

Verify acceptance: Make sure it works on the platforms you regularly use

Review limits: Does the card offer sufficient spending limits for your needs?

For most Nigerians, the ideal virtual dollar card combines low fees, easy funding options, wide acceptance, and reliable customer support.

FAQs

Are virtual dollar cards legal in Nigeria?

Yes, they are completely legal. These cards are provided by licensed financial institutions that comply with Central Bank of Nigeria regulations.

Can I use a virtual dollar card on any website?

Most virtual dollar cards work on major international platforms. However, some websites might have restrictions based on geographic location rather than the card type itself.

How do I fund a virtual dollar card?

Most providers allow you to fund the card through their app or website. You typically convert Naira to USD at the provider’s exchange rate, and the funds are then available on your virtual card.

What happens if my virtual card is compromised?

One of the advantages of virtual cards is that you can easily freeze or delete them if you suspect any unauthorized use. Most providers allow you to do this directly from their app.

Can I have multiple virtual dollar cards?

Yes, many providers allow you to create multiple virtual cards for different purposes. This can be useful for separating business expenses from personal spending or for managing different subscription services.

How do I get a virtual card in Nigeria?

To get a virtual card in Nigeria, you need to sign up with a fintech platform or bank that offers virtual cards. Some popular options include Grey, ALAT by Wema, Cardtonic, Chipper Cash, and Eversend. After signing up, navigate to the virtual card section, complete any necessary verification, and fund your account to generate a virtual card.

How much is an ALAT virtual dollar card in Nigeria?

ALAT by Wema offers a virtual dollar card, but the cost depends on the exchange rate at the time of funding. Typically, you may need to pay an issuance fee and maintain a minimum balance. It’s best to check the ALAT app or website for the most updated charges.

Does OPay work in Ghana?

No, OPay does not currently operate in Ghana. It primarily serves users in Nigeria for payments, transfers, and financial services.

Does UBA offer virtual cards?

Yes, UBA offers virtual cards, such as the UBA Dollar Virtual Card, which can be used for online transactions. Customers can request a virtual card through UBA’s mobile banking app or online banking platform.

What is the difference between an OPay physical card and a virtual card?

An OPay physical card is a tangible debit card that can be used for ATM withdrawals, POS transactions, and online payments. A virtual card, on the other hand, exists only in digital form and is mainly used for online transactions, providing extra security since it cannot be lost or stolen physically.

Beyond The Basics: Advanced Virtual Card Strategies

Once you’re comfortable using virtual dollar cards, consider these advanced strategies:

Create separate cards for different services: Use dedicated cards for various subscriptions to better track spending

Set spending limits: Many providers allow you to set limits on individual cards

Use virtual cards for trial subscriptions: Create a card with just enough funds for the trial to avoid unexpected charges

Monitor exchange rates: Fund your card when rates are favorable to maximize value

Consider specialized cards: For business advertising or specific uses, look at cards designed for those purposes

As Nigeria continues its digital transformation, virtual dollar cards will become even more integral to how we participate in the global digital economy. The technology is evolving rapidly, with providers continuously improving features, reducing fees, and enhancing security.

For Nigerians looking to access international services or participate in the global marketplace, virtual dollar cards have removed a significant barrier. They’ve democratized access to international payments, enabling everything from educational opportunities through platforms like Coursera to business growth via advertising on platforms like Facebook and Google.

Whether you’re a student, freelancer, business owner, or just someone who enjoys shopping on international websites, there’s a virtual dollar card solution that fits your specific needs. The key is understanding your requirements and matching them to the provider that offers the best value proposition for your particular situation.

The options listed in this guide represent the best available currently, but the market is dynamic. New providers emerge regularly, and existing ones frequently update their offerings. Always do a quick check for the most current information before making your final decision.

With the right virtual dollar card in your digital wallet, you’re all set to participate fully in the global digital economy – no barriers, no limitations, just smooth international transactions at your fingertips.

Nigeria’s fintech industry is booming, and it’s changing the way people handle money. Whether you’re sending money to a friend, paying for groceries, or even saving for the future, these fintech companies make it easier, faster, and often cheaper. Let’s break down some of the biggest players in Nigeria’s fintech space right now.

1. Grey

Grey makes it easy for Nigerians to receive payments from international clients. Imagine you’re a freelancer working for a company abroad—you don’t want the hassle of traditional banks delaying your money. Grey gives you a virtual foreign account so you can receive dollars, euros, or pounds and convert them to naira instantly.

2. Paystack

If you’ve ever bought something online in Nigeria, chances are you’ve used Paystack. It helps businesses accept payments from customers via cards, bank transfers, and even USSD. It’s like a digital cash register that businesses can rely on to get paid smoothly.

3. Opay

Opay is like a one-stop shop for financial services. You can use it to send and receive money, pay bills, buy airtime, and even take a loan. Plus, they have a ride-hailing and food delivery service. Think of it as a digital bank mixed with a mini marketplace.

4. PalmPay

PalmPay is another mobile money app that makes transactions easy. It’s known for its cashback rewards—so every time you pay for something, you might get a little money back. It’s like earning small change every time you shop!

5. MoMoPSB

Short for Mobile Money Payment Service Bank, MoMoPSB is MTN’s way of helping people send and receive money without a bank account. If you have an MTN line, you can access their services through USSD codes, making it super convenient for people without smartphones.

6. Kuda

Kuda is a full-fledged digital bank. Unlike traditional banks, it has no physical branches, meaning you can do everything from your phone. No hidden charges, no unnecessary fees—just simple banking.

7. Moniepoint

Moniepoint helps businesses accept payments easily. If you’ve ever paid with a POS machine at a small shop, it might have been Moniepoint’s. It also provides loans and banking solutions to small businesses.

8. Fincra

Fincra specializes in cross-border payments. If a business wants to send or receive money internationally, Fincra makes sure it happens quickly and smoothly. It’s a big deal for Nigerian companies that deal with foreign customers.

9. Paga

Paga is one of Nigeria’s oldest fintech companies. It lets you send money, pay bills, and make purchases without needing a bank account. Think of it as a digital wallet that works for everyone.

10. Carbon

Carbon isn’t just a payment platform; it also offers loans, savings, and investment options. If you need quick cash for an emergency, Carbon can lend you money without the long wait times of traditional banks.

11. FairMoney

Like Carbon, FairMoney is a digital lender that gives quick loans with minimal paperwork. It also has a banking service where you can open an account and save money.

12. Eversend

Eversend is a multi-currency wallet that allows users to send and receive money in different currencies. If you travel a lot or make international purchases, Eversend helps you manage foreign exchange rates easily.

13. Cowrywise

Cowrywise helps people save and invest their money wisely. It’s like a digital piggy bank that also grows your money by investing it in stocks, bonds, and other financial tools.

14. PiggyVest

PiggyVest is another savings and investment platform that helps Nigerians develop better money habits. It allows you to lock away funds so you don’t spend them impulsively. Piggyvest was co-founded by Odunayo Eweniyi, one of the most influential Nigerian women in Tech.

15. Remita

Remita is widely used by businesses and government agencies for managing payments. Whether it’s paying salaries, processing taxes, or handling large transactions, Remita makes sure the money moves efficiently.

16. Chipper Cash

Chipper Cash focuses on free and low-cost money transfers across Africa. If you need to send money to someone in Ghana or Kenya, for example, Chipper Cash makes it super easy and affordable.

17. Flutterwave

Flutterwave is one of Nigeria’s biggest fintech success stories. It provides payment solutions for businesses of all sizes, helping them accept payments from customers all over the world. Whether it’s a small business selling clothes on Instagram or a big company, Flutterwave makes payments seamless.

Nigeria’s fintech industry is changing the way people interact with money. Whether you need a loan, want to save, or run a business, there’s a fintech company designed to help. As these companies continue to grow, banking and finance will only get easier for Nigerians. Which one do you use the most?

A former high-ranking executive at Kuda, one of Nigeria’s prominent fintech startups, has taken legal action in the United Kingdom, alleging workplace discrimination, a toxic corporate culture, and wrongful termination. Rosemary Hewat, Kuda’s former Group Chief People Officer, filed a lawsuit claiming that the company and its CEO, Babatunde Ogundeyi, fostered an environment where women were marginalized and treated unfairly.

According to reports from credible sources, court documents indicate that Hewat alleges Kuda failed to grant her stock options under the same terms as her male counterparts and dismissed her after she raised concerns about gender-based workplace mistreatment.

Kuda, an FCCPC-approved loan app in Nigeria that has publicly positioned itself as a proponent of gender inclusivity, now faces scrutiny over these claims. The company, backed by Target Global, has highlighted its efforts to support women in the workplace. Hewat herself played a key role in these initiatives, announcing in March 2023 that Kuda had achieved a 1:1 gender ratio. However, her lawsuit paints a different picture, describing an environment where women were systematically excluded and belittled.

Hewat specifically accuses Ogundeyi of fostering a hostile work culture. The lawsuit claims he made demeaning remarks about female employees, publicly humiliated two women at a strategy retreat in December 2023, and dismissed them as “low class” for lacking exposure to luxury. She further alleges that he instilled fear among employees, stating that staff “see him as God” and are afraid to approach him.

When asked about the allegations, Kuda confirmed the lawsuit but declined to comment.

“In line with our current policy and out of respect for privacy, we do not comment on matters of this nature involving current or former employees,” a Kuda spokesperson stated via email.

One of the key points in Hewat’s legal claims revolves around her Employee Stock Ownership Plan (ESOP). She alleges that Kuda reneged on an agreement to grant her shares at the more favorable Series A valuation, instead offering them at the higher Series B price. Meanwhile, her male counterpart, Steven Bastian, reportedly received adjusted terms to reflect the lower valuation. According to the lawsuit, Ogundeyi justified this by claiming Bastian’s role as Group CFO was “more important” than Hewat’s.

Hewat also asserts that she faced professional retaliation after voicing her concerns. She says she was deliberately excluded from critical meetings, and that Kuda’s Group Chief Operating Officer, Pavel Khristolubov, gradually took over aspects of her role while undermining her. When she raised the issue with Ogundeyi, she claims he dismissed her concerns and advised her to “spend the next six months getting Khristolubov to like her.”

Her employment at Kuda officially ended on February 20, 2024—just weeks after she filed a formal grievance about the ESOP issue. Hewat alleges she was dismissed while on her way to an executive retreat in Nigeria, with Kuda framing the decision as part of cost-cutting measures. However, she argues that the company continued spending on discretionary items, including allegedly employing a nanny for Ogundeyi’s children at the company’s expense. Adding to the confusion, Kuda’s Chief Technical Officer, Mutairu Mustapha, reportedly told Hewat that her termination was a “mistake” and urged her to return to work.

The impact of these events, Hewat claims, severely affected her mental and physical health, leading to panic attacks, depression, and insomnia. She is now seeking financial compensation for lost benefits, emotional distress, and punitive damages for what she describes as severe workplace misconduct.

Kuda has yet to issue a public statement addressing the lawsuit or the allegations made against its leadership.

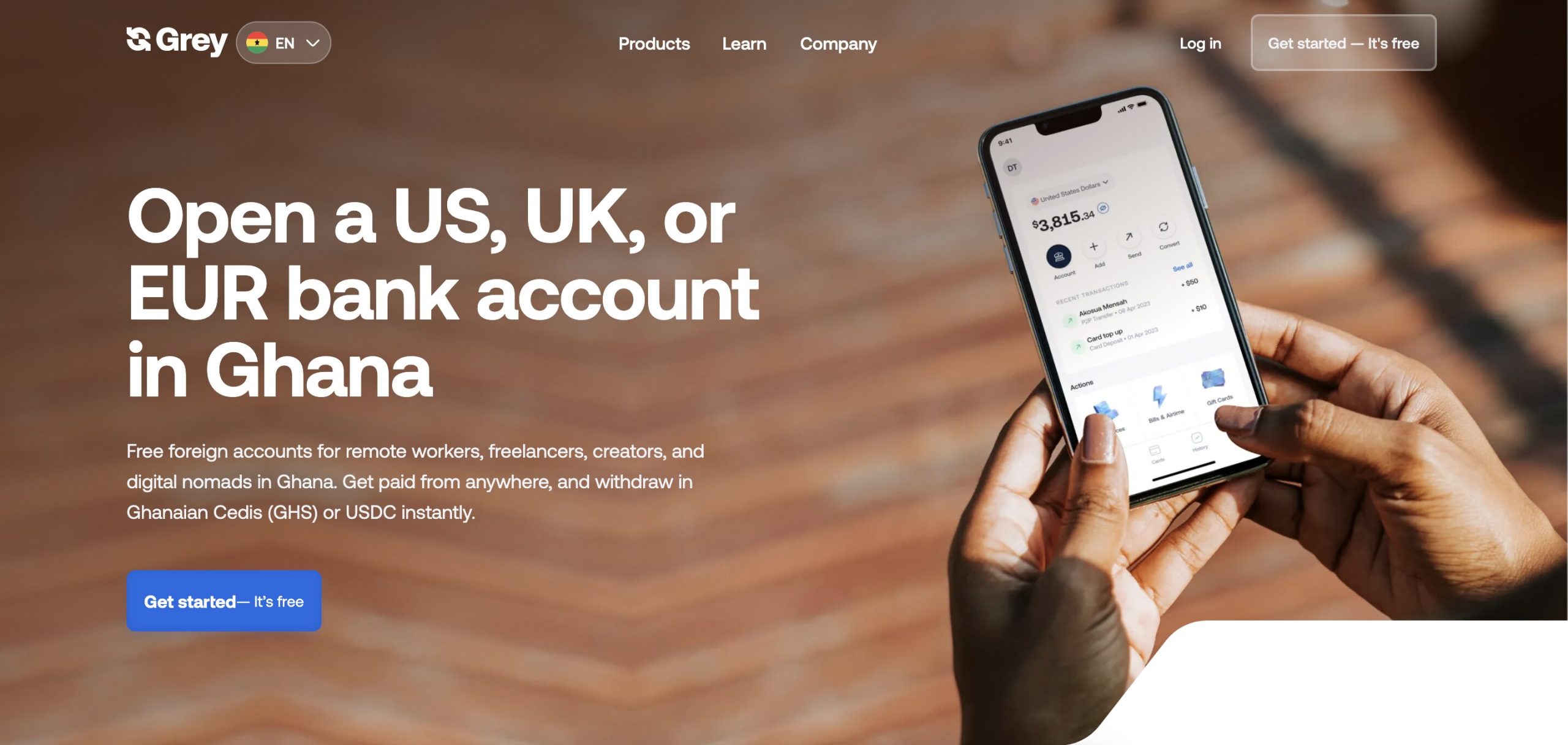

Need an Easy Way to Receive International Payments?

Imagine you’re a freelancer in South Africa, and a client from the U.S. wants to pay you in dollars. Or maybe you run an online store, and international customers prefer paying in euros or pounds. Normally, you’d deal with slow bank transfers, high fees, and exchange rate confusion. But what if you had a simple way to receive and manage foreign currencies right from South Africa?

That’s where Grey comes in! Grey lets you open a US, UK, or EU foreign bank account from South Africa, making it easy to receive international payments, exchange currencies, and withdraw in South African Rand (ZAR)—all without the usual banking headaches.

Let’s dive into how you can open a Grey foreign account today!

What is Grey, and Why Should You Use It?

Grey is a fintech platform that provides foreign bank accounts without the hassle of traditional banks. With Grey, you can open a USD, GBP, or EUR account in minutes—no need to travel or deal with complicated paperwork.

Here’s what you can do with a Grey foreign account:

Receive money from international clients easily

Convert foreign currency to ZAR at competitive rates

Withdraw to your local South African bank account instantly

Use virtual cards for online payments in different currencies

Basically, it’s like having a bank account in the U.S., U.K., or Europe—without leaving South Africa!

Why Open a Foreign Bank Account With Grey?

Grey makes international banking simple, fast, and affordable. Here’s why South Africans are using Grey:

Get paid like a local in multiple currencies – Receive payments in USD, GBP, or EUR directly into your foreign bank account.

Instant withdrawals to South African Rand (ZAR) – No more long wait times to access your funds.

No hidden fees – Traditional banks charge unnecessary fees, but Grey is transparent and cost-effective.

Virtual cards for international payments – Need to pay for global services like Netflix, Amazon, or Spotify? Grey makes it easy.

Perfect for freelancers, remote workers, and businesses – If you earn or spend in foreign currencies, Grey helps you save time and money.

How to Open a Foreign Bank Account in South Africa With Grey (3 Simple Steps!)

Unlike traditional banks that require tons of paperwork, Grey’s process is fully online and takes just a few minutes. Here’s how to get started:

Step 1: Sign Up on Grey

Visit Grey’s website or download the Grey mobile app. Create an account using your name, email, and phone number—it’s just like signing up for any other online service.

Step 2: Complete KYC Verification

To keep everything secure, Grey requires a quick verification process. You’ll need to:

Upload a government-issued ID (South African ID, Passport, or Driver’s License)

Take a quick selfie for identity verification

Provide proof of address (like a bank statement or utility bill)

This process ensures that your account is secure and compliant with regulations.

Step 3: Get Your Foreign Bank Account

Once verified, Grey provides you with a foreign bank account (USD, GBP, or EUR), and you’re good to go! Now, you can send and receive international payments like a pro.

How to Use Your Grey Foreign Bank Account

Now that you have your foreign account, here’s how to make the most of it:

1. Receive Payments From Anywhere

Freelancers, remote workers, and businesses can share their Grey account details with international clients and get paid seamlessly.

2. Convert and Withdraw Money Easily

Got paid $500 in your Grey USD account? Convert it to ZAR at competitive exchange rates and withdraw it instantly to your local South African bank account.

3. Make International Payments

Need to buy software, subscribe to services, or shop online? Use Grey’s virtual cards to make payments in foreign currencies without restrictions.

Frequently Asked Questions About Grey

1. Is Grey a Bank?

No, Grey is a fintech platform that partners with licensed financial institutions to provide foreign bank accounts and payment services.

2. Is Grey Safe?

Yes! Grey uses encryption, identity verification, and other security measures to protect your money and personal data.

3. How Long Does It Take to Open an Account?

Signing up takes just a few minutes, and KYC verification is usually completed within a few hours.

4. Are There Any Hidden Fees?

Nope! Grey is transparent with its fees, and you’ll always see the exchange rates before making a conversion.

Why You Should Open a Grey Foreign Account Today

If you earn or spend money in multiple currencies, Grey is the easiest way to manage international transactions from South Africa.

No paperwork. No hidden fees. Works anywhere in South Africa. Instant withdrawals.

Ready to simplify your international banking? Sign up on Grey today and start managing your foreign payments effortlessly!

Fincra, a leading B2B payment infrastructure provider, has appointed Emmanuel Babalola as its new Chief Commercial and Growth Officer. This move comes as the company refines its strategy to scale cross-border transactions and expand its reach.

Babalola brings a wealth of experience in fintech and crypto. He previously served as CEO of Bundle, a social payments app for cash and cryptocurrency, before it pivoted in July 2023 to focus solely on its peer-to-peer platform, Cashlink. Before that, he was the Director for Africa at Binance, the world’s largest cryptocurrency exchange.

Fincra CEO Wole Ayodele expressed confidence in Babalola’s ability to drive the company forward. “His track record of scaling platforms, driving innovation, and advocating for financial inclusion aligns perfectly with our mission to build seamless payment rails for Africa. His leadership will be instrumental as we continue to push boundaries and redefine payments across the continent.”

Founded in 2021, Fincra provides APIs that help fintechs develop and scale payment solutions. Since 2023, the company has processed over $10 billion in transactions and serves clients such as Lemfi, OneLiquidity, and Cleva. It also offers an API designed to help Nigerian businesses collect local payments through bank transfers and card transactions. Operating in multiple regions—including Ghana, South Africa, Kenya, Uganda, the UK, Europe, and North America—Fincra is now eyeing expansion into Francophone Africa.

Babalola sees his new role as an opportunity to further his mission of financial empowerment. “Africa’s financial ecosystem is evolving rapidly, and Fincra is at the forefront of building the payment infrastructure powering the next generation of businesses and entrepreneurs. My mission has always been to enable freedom and prosperity for Africa through technology, and joining Fincra is an exciting opportunity to amplify this vision.”

With this leadership addition, Fincra is positioning itself to accelerate growth and innovation in Africa’s digital payment space.

Raenest, a Nigerian fintech specializing in cross-border payments, has secured $11 million in a Series A funding round, bringing its total funding to $14.3 million. The investment will support its expansion into new markets and the introduction of additional financial tools.

The round was led by QED Investors, with backing from Norrsken22, Ventures Platform, P1 Ventures, and Seedstars. This follows Raenest’s earlier funding rounds, including a $700,000 pre-seed round in 2022 and a $2.6 million seed round in 2023.

Expansion Plans and New Features

With operations in Kenya, Ghana, Tanzania, and Uganda, Raenest is now eyeing launches in Egypt and the U.S. The company also plans to roll out new offerings such as expense management, savings, and investment tools to enhance its multi-currency payment solutions.

This investment reflects the growing confidence in African fintech startups. In January 2025 alone, African startups secured $289 million in funding—a staggering 240% increase from the previous year. Notable fintech investments include Moniepoint’s $10 million from Visa and LemFi’s $53 million round.

From Employer of Record to Fintech Powerhouse

Since its launch in 2022, Raenest has transitioned from an Employer of Record (EOR) to a full-fledged fintech platform. It helps freelancers and businesses receive international payments, convert currencies, and manage multi-currency wallets. Users can open global bank accounts, access physical and virtual dollar cards, and transact in USD, EUR, and GBP.

Through its consumer-focused product, Geegpay, Raenest enables freelancers, content creators, and solopreneurs to receive payments from platforms like Upwork, Fiverr, and Gusto. The company reports serving over 700,000 users and processing more than $1 billion in transactions.

Africa’s gig economy is expanding at an annual rate of 20%, yet freelancers and businesses continue to face challenges with cross-border payments. Investors see Raenest as a key player in bridging this gap.

“Africa’s gig economy is growing at an impressive 20% year-on-year, yet cross-border payment challenges persist for workers and businesses alike. Our investment in Raenest reflects our belief that they are unlocking new opportunities by transforming how Africa’s global workforce connects to the world economy,” said Lexi Novitske, General Partner of Norrsken22.

Business Banking and Competitive Edge

In March 2024, Raenest launched its business banking service, quickly positioning itself as a go-to alternative for African startups that lost access to Mercury, a U.S.-based banking provider. According to CEO Alade, the company is profitable and serves around 300 businesses, including Moniepoint, Helium Health, Fez Delivery, and Matta. Since its launch, Raenest’s business banking arm has processed over $100 million in transactions.

Raenest operates in an increasingly competitive cross-border payment space, facing off against Cleva, Grey, and LemFi. However, its ability to serve both businesses and individuals gives it a unique position in the market. While its primary focus has been on Africans living within the continent, Raenest is now looking to extend its reach to Africans in the diaspora as well.

“The mission is to become a trusted financial platform that makes it easier for people to manage their funds globally,” Alade said.

With its latest funding, Raenest is poised to scale further, reinforcing its role in Africa’s evolving digital payments landscape.

Investing is like planting a tree. You put money in, take care of it, and over time, it grows into something valuable. But just like you wouldn’t plant a tree without checking if the soil is good, you shouldn’t invest without choosing the right platform.

Nigeria has many investment apps promising great returns, but how do you know which ones you can trust? Don’t worry—I’ve got you covered. In this guide, I’ll break down the best investment apps in Nigeria, explaining what they do, how they work, and what makes them worth your time. Let’s dive in!

1. Cribstock

Cribstock is changing the way Nigerians invest in real estate. Instead of needing millions to buy a house or apartment, you can invest in property with as little as N10,000. The platform allows users to own shares in rental properties and earn passive income from rent payments. It’s a great option for those looking to grow wealth through real estate without the hassle of buying or managing properties themselves.

2. PiggyVest

Founded by Odunayo Eweniyi, PiggyVest started as a savings platform but now offers investment opportunities through its Investify feature. With as little as N5,000, you can invest in fixed income, agriculture, and transportation sectors and earn up to 25% returns. If you’re also looking for a way to save money effectively, PiggyVest offers an automatic savings plan with interest rates between 5% and 15% per year.

3. Carbon

Formerly known as Paylater, Carbon is a digital bank that also offers great investment options. It provides three investment plans:

Cash Vault: Lock your money away and earn 11% interest.

FlexSave: A flexible plan with up to 9% interest.

Goals Plan: Set daily, weekly, or monthly targets and earn 9.5% interest. If you’re looking for a mix of digital banking and investment, Carbon is a solid choice.

4. Cowrywise

Cowrywise helps users invest in naira and dollar mutual funds. If you don’t want to put all your eggs in one basket, this app allows you to spread your investments across multiple assets. It also offers different savings plans, including emergency funds and halal savings for ethical investors. Plus, there are no minimum withdrawal restrictions.

5. Bamboo

Bamboo gives Nigerians access to over 3,500 local and international stocks. You can invest in the Nigerian Stock Exchange or major U.S. stock markets. The app’s security features ensure that your investments are safe, and you can start with as little as $20.

6. Trove

Trove is another great app for stock investing. With as little as N1,000, you can buy shares in Nigerian, American, and Chinese companies. It also supports investments in bonds, ETFs, and real estate investment trusts (REITs), making it a versatile option for those looking to diversify their portfolio.

7. Risevest

Risevest focuses on dollar-denominated investments, allowing Nigerians to invest in U.S. stocks, real estate, and Eurobonds. The app boasts an average return of 14% on stock investments, although actual returns depend on market performance. With a minimum investment of just $10, it’s a great way to protect your money from naira fluctuations.

8. Chaka