In today’s globalized economy, digital payments have become crucial for international transactions and e-commerce. Platforms like PayPal simplify online purchases, making them accessible and secure. However, despite the widespread adoption of PayPal around the world, it remains notably absent in some countries, including Ghana. This article explores the various factors contributing to the absence of PayPal services in Ghana, and how it affects the local economy and tech sector.

Historical Context and Current Landscape

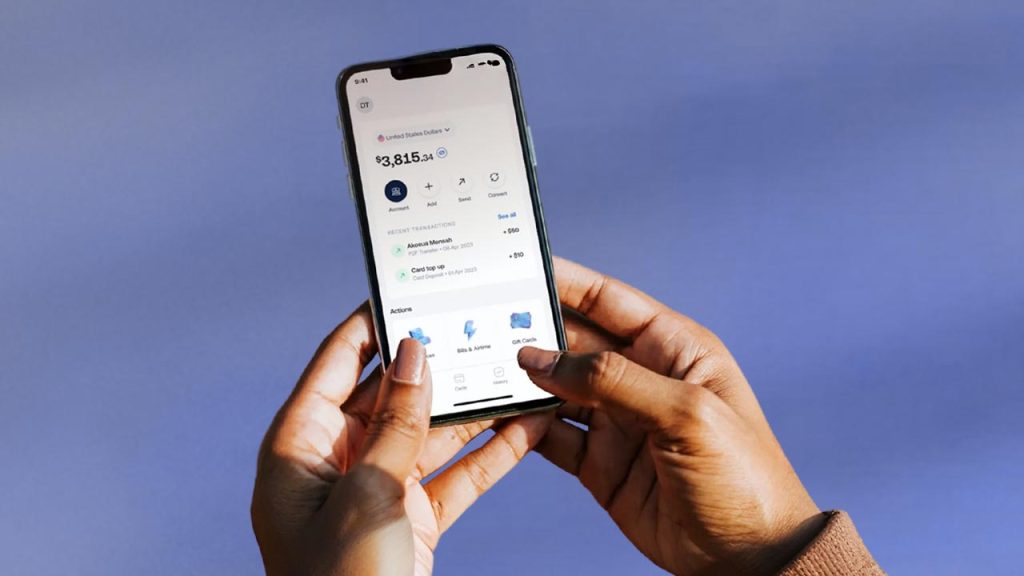

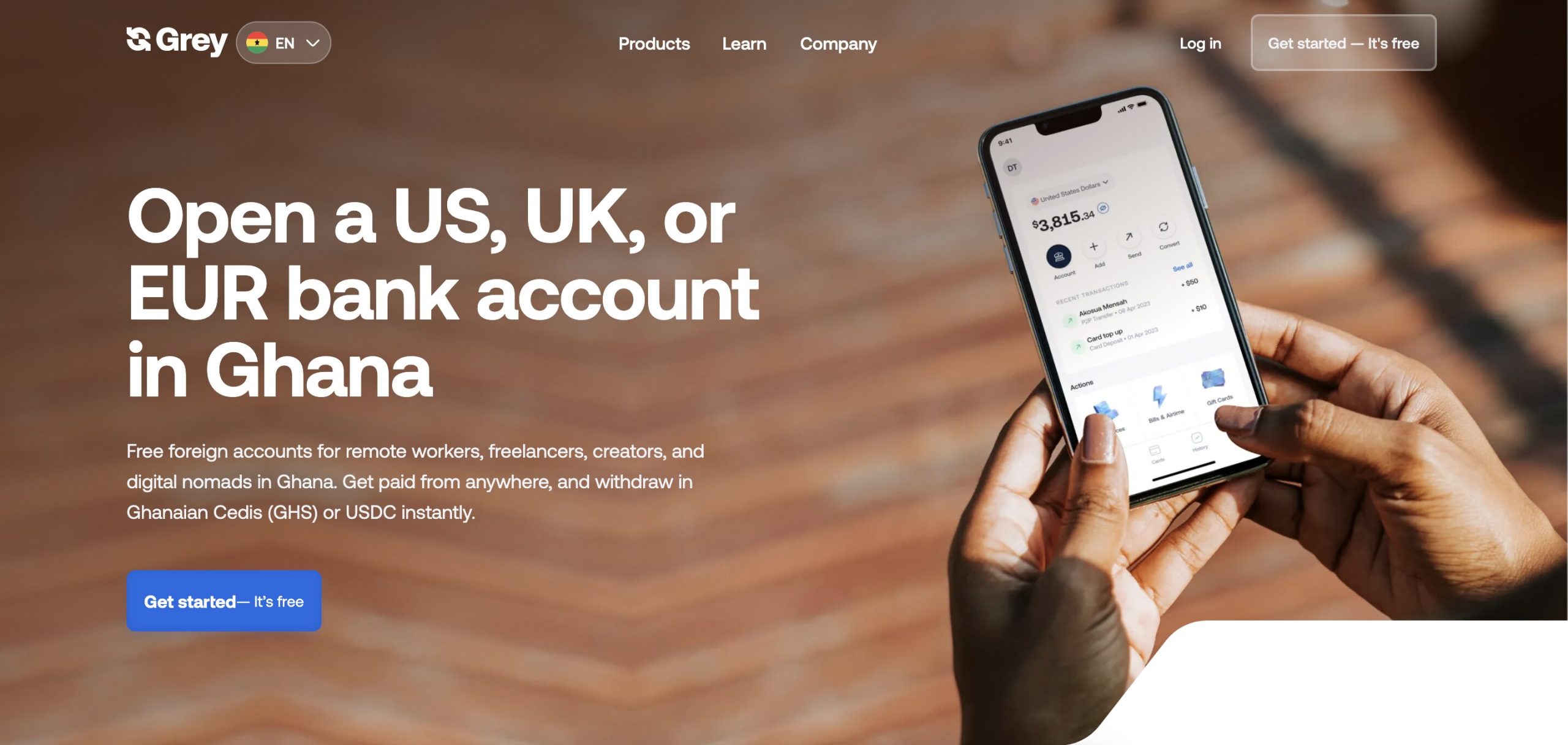

Ghana has seen significant technological advancements and has a burgeoning e-commerce sector. With a growing middle class and increasing internet penetration, the demand for digital payment solutions is higher than ever. Mobile money services like MTN Mobile Money, Vodafone Cash (now Telecel Cash), and AirtelTigo Money have filled this gap to some extent but lack the global reach and user base of PayPal.

Regulatory Challenges

One of the primary reasons why PayPal has not yet entered the Ghanaian market is the complex regulatory environment. Financial regulations in Ghana are designed to control money laundering and ensure the stability of the financial system. PayPal, with its global operations, must ensure that it complies with these regulations comprehensively before it can operate in Ghana. This involves navigating both local regulations and international financial laws, which can be time-consuming and costly.

Economic Factors

Another significant factor is the economic environment. While Ghana’s economy is growing, issues such as currency stability and inflation pose risks for international financial service providers. PayPal typically operates in markets where there is a certain level of economic stability to mitigate potential financial losses that could arise from currency fluctuations.

Market Viability

For PayPal, the decision to enter a new market also depends on the market’s profitability potential. This includes the number of potential users and the volume of transactions. Despite the high demand for such services in Ghana, the current volume and value of digital transactions may still be deemed insufficient by PayPal to warrant the establishment of services, especially considering the costs associated with setting up and maintaining operations.

Financial Infrastructure

The financial infrastructure in Ghana, though improving, is still developing. The readiness of the banking system to integrate with international payment platforms like PayPal is crucial. This integration involves technological upgrades and compliance with international security standards, which are still underway in many Ghanaian banks.

Risk of Fraud

The risk of financial fraud is a concern for any financial service provider. In regions where digital fraud tactics are prevalent, PayPal might be cautious in rolling out its services to mitigate potential losses. Ensuring that robust security measures are in place is a prerequisite for PayPal’s operations, which could delay its introduction in such markets.

Alternative Solutions and the Future

In the absence of PayPal, other services have been gaining traction in Ghana. These include other international payment platforms like Skrill, Payoneer, and local innovations that provide similar services. The Ghanaian government and financial institutions continue to work towards improving financial regulations and infrastructure, which could pave the way for PayPal in the future.

Frequently Asked Questions (FAQs)

Q: Why is PayPal not available in Ghana?

PayPal is not available in Ghana primarily due to regulatory challenges, economic factors, market viability concerns, the developing financial infrastructure, and the risks associated with financial fraud.

Q: How does the absence of PayPal affect the Ghanaian economy?

The absence of PayPal limits the options for international e-commerce and may slow the growth of Ghana’s digital economy by making it more difficult for businesses and freelancers to engage with global markets.

Q: What are the alternatives to PayPal in Ghana?

Alternatives to PayPal in Ghana include other international payment services like Skrill and Payoneer, as well as local mobile money services that support international transactions.

Q: Is there a possibility of PayPal entering the Ghanaian market soon?

While it is difficult to predict, the possibility exists if Ghana continues to improve its financial regulations and infrastructure, and if economic conditions stabilize to meet PayPal’s operational standards.

Q: What can be done to expedite PayPal’s entry into Ghana?

Efforts can be made to strengthen financial regulations, enhance the security and infrastructure of the banking system, and ensure economic stability to create a more favorable environment for international payment platforms like PayPal.

Q: Which African countries is PayPal available in?

As of 2024, PayPal is available in several African countries, including South Africa, Kenya, Morocco, Egypt, Nigeria, Algeria, Angola, Benin, Botswana, Burkina Faso, Burundi, Cameroon, Cape Verde, Chad, Comoros, Ivory Coast, Democratic Republic of the Congo, Djibouti, Eritrea, Ethiopia, Gabon Republic, Gambia, Guinea, Guinea-Bissau, Lesotho, Madagascar, Malawi, Mali, Mauritania, Mauritius, Mozambique, Namibia, Niger, Republic of the Congo, Rwanda, Saint Helena, São Tomé and Príncipe, Senegal, Seychelles, Sierra Leone, Swaziland, Tanzania, Togo, Tunisia, Uganda, Zambia, and Zimbabwe. These countries allow residents to open and operate a PayPal account for secure international payments and money transfers.

Q: Which other African countries is PayPal not available in?

PayPal is not available in some African countries due to various regulatory and operational constraints. Notable exclusions include Libya, Sudan, and Somalia. In these countries, residents cannot officially open or operate a PayPal account, limiting their access to this global payment platform.

Understanding why PayPal is not yet available in Ghana provides insight into the complexities of financial services in emerging markets and highlights the need for ongoing improvements in financial infrastructure and regulations to support economic growth and global integration.